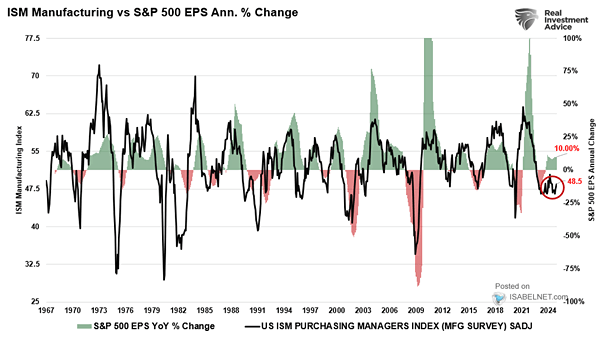

ISM Manufacturing Index vs. S&P 500 Index

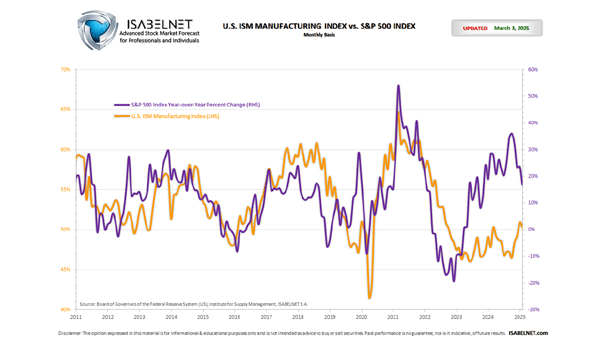

ISM Manufacturing Index vs. S&P 500 Index The U.S. ISM Manufacturing Index in June stands at 49.0%, above the consensus forecast of 48.8%, which is indicative of a contraction in the manufacturing sector. This chart shows the correlation between the U.S. ISM manufacturing index and the S&P 500 index year-over-year percent change, since 2011. Click…