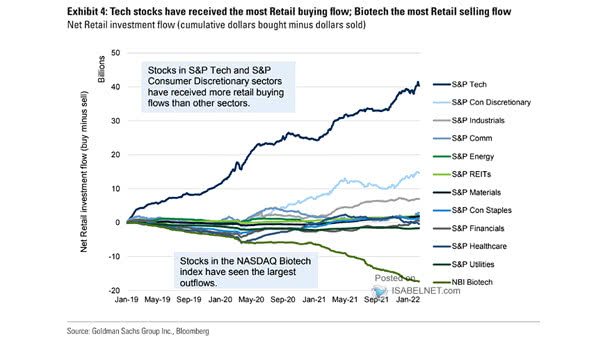

3-Month Rolling S&P 500 Retail Flows

3-Month Rolling S&P 500 Retail Flows Retail traders have demonstrated robust buying activity in recent months, with Goldman Sachs estimating net purchases of approximately $20 billion in U.S. stocks over the past three months. Image: Goldman Sachs Global Investment Research