Stocks, Bonds, Foreign Exchange and Commodities Outperformance

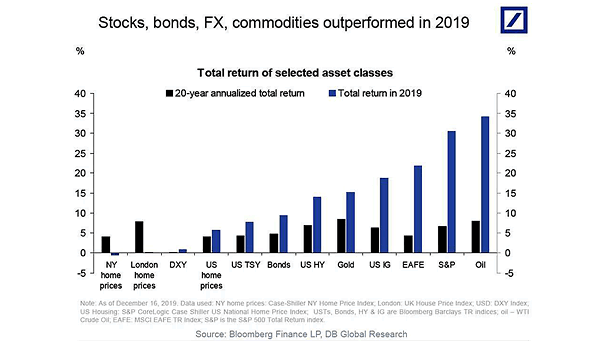

Stocks, Bonds, Foreign Exchange and Commodities Outperformance Stocks, bonds, FX and commodities outperformed in 2019. Image: Deutsche Bank Global Research

Stocks, Bonds, Foreign Exchange and Commodities Outperformance Stocks, bonds, FX and commodities outperformed in 2019. Image: Deutsche Bank Global Research

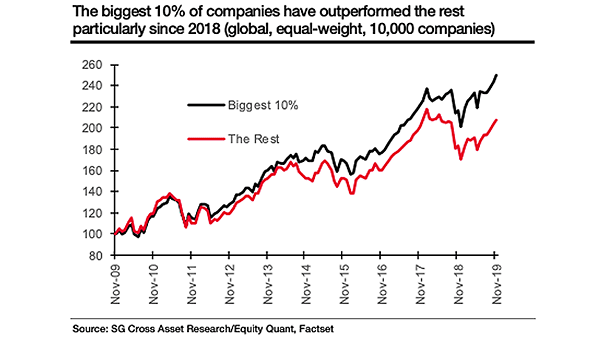

Outperformance of the Biggest 10% Companies vs. Rest of the Market Chart showing that the biggest 10% of companies have significantly outperformed the rest of the market. Image: Societe Generale Cross Asset Research

S&P 500 and Large-Cap Funds Outperformance Over Benchmarks Only 28% of large-cap funds are outperforming their benchmarks this year. Image: Goldman Sachs Global Investment Research

U.S. Equity Market Outperformance According to Gavekal, U.S. outperformance is mainly cyclical, not structural, and best investment opportunities could be in non-US assets. Image: Gavekal, Macrobond

Hedge Fund Industry Outperformance – Negative over Past Decade The chart below shows how it’s hard to beat the market over time. Image: Greenline Partners LLC

Performance – Value vs. Growth The U.S. market is experiencing outperformance in growth sectors driven by innovation and strong earnings, whereas value sectors dominate outside the U.S. due to slower earnings growth and differing economic dynamics. Image: Goldman Sachs Global Investment Research

U.S. Small-Cap Stocks – Russell 2000 vs. S&P 500 While U.S. small-cap stocks have notably underperformed large caps for an extended period, history suggests that such cycles are not unusual and are often followed by multi-year stretches of small-cap outperformance. Image: Bloomberg

% of Large-Cap Mutual Funds Outperforming their Benchmarks Active large-cap funds are having a good year in 2025, with half of them beating their benchmarks so far—much higher than the average of 37%. Still, history shows that it’s uncommon for this outperformance to last. Image: Goldman Sachs Global Investment Research

Median Excess Return vs. S&P 500 on Day After Earnings Report While positive earnings surprises still led to outperformance in 1Q, the magnitude of that outperformance was smaller than usual for the quarter, due to broader macroeconomic concerns or already high expectations priced into stocks. Image: Goldman Sachs Global Investment Research

World Technology vs. World Ex. TMT Continuous technological innovation, resilience, and the expanding societal dependence on technology strongly underpin the tech sector’s prospects for sustained market outperformance. Image: Goldman Sachs Global Investment Research

YTD Equity Return vs. U.S. In 2025, the relative outperformance of international stocks compared to U.S. equities has underscored the benefits of diversification for investors so far. Image: Goldman Sachs Global Investment Research