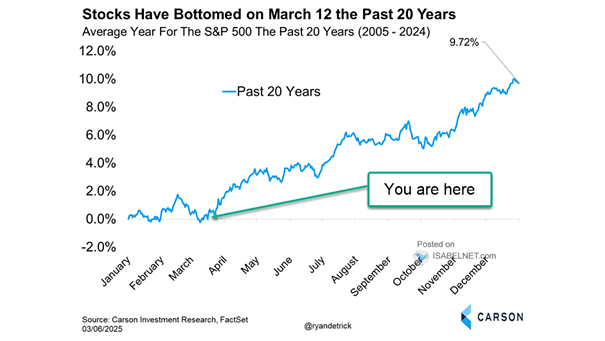

Average Year for the S&P 500 the Past 20 Years

Average Year for the S&P 500 the Past 20 Years Over the past two decades, March 12 has often marked the bottom for U.S. stocks, with rebounds taking shape soon after. History doesn’t always repeat itself, but investors know it tends to rhyme. Image: Carson Investment Research