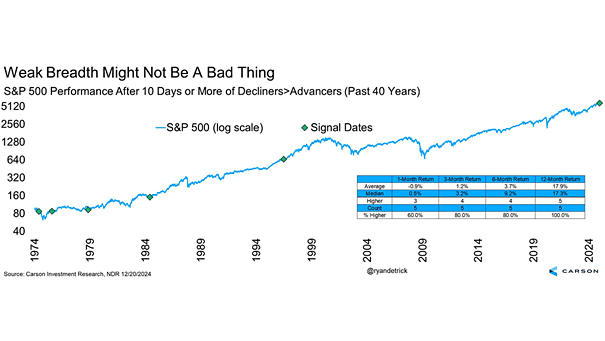

S&P 500 Performance After 10 Days or More of Decliners > Advancers

S&P 500 Performance After 10 Days or More of Decliners > Advancers Bulls are smiling again! Since 1974, when the S&P 500 had more decliners than advancers for 10 or more consecutive days, it has been positive 100% of the time over the following 12 months, with an average gain of 17.9%. Image: Carson Investment…