ISABELNET Cartoon of the Day

ISABELNET Cartoon of the Day With Bitcoin surpassing $100,000, bears are now on dating apps looking for a bull! Have a Great Day, Everyone! 😎

ISABELNET Cartoon of the Day With Bitcoin surpassing $100,000, bears are now on dating apps looking for a bull! Have a Great Day, Everyone! 😎

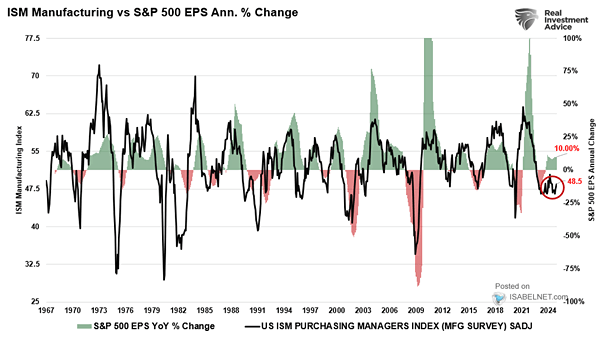

U.S. ISM Manufacturing Index vs. S&P 500 EPS Annual % Change With the ISM Manufacturing Index still in contraction territory and strongly correlated with S&P 500 earnings growth, questions arise about the resilience of corporate earnings in 2025. Image: Real Investment Advice

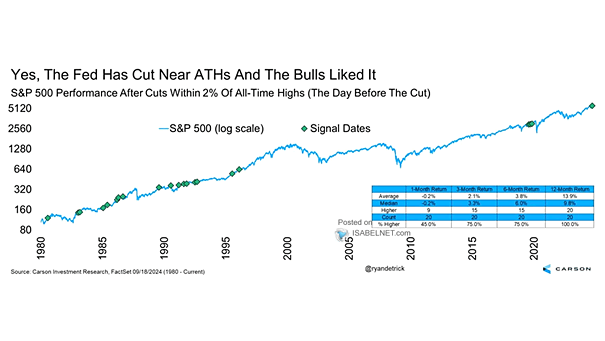

S&P 500 Performance After Fed Cuts Within 2% of All-Time Highs Bulls rejoice! Since 1980, when the S&P 500 was within 2% of its all-time high during a Fed rate cut, it has been positive 100% of the time over the following 12 months, with an average gain of 13.9%. Image: Carson Investment Research

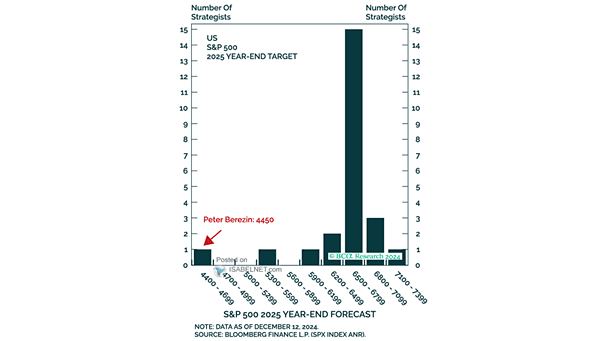

S&P 500 2025 Year-End Target While most strategists project a bullish 2025 for the S&P 500, a notable minority advocates for caution. This divergence in opinion could comfort investors wary of market euphoria. Image: BCA Research

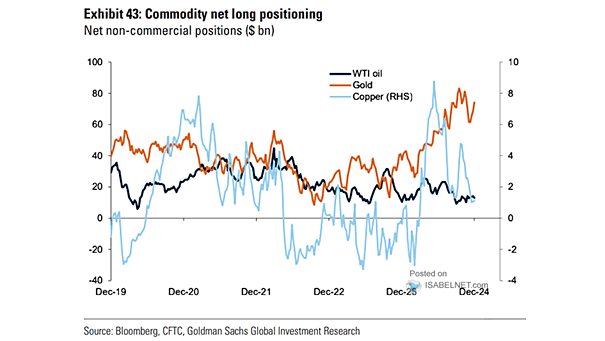

Commodities (Oil, Gold, Copper) – Commodity Net Long Positioning While there are some pressures from rising U.S. Treasury yields and a stronger U.S. dollar, the current landscape for gold positioning is marked by a robust bullish sentiment, with increasing net long positions. Image: Goldman Sachs Global Investment Research

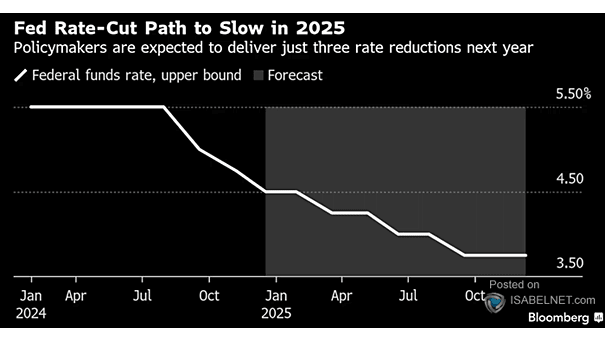

Interest Rates – Implied Fed Funds Target Rate The Fed is likely to cut rates by 25 basis points today, but projections for 2025 indicate a more gradual easing strategy, aiming to boost the economy while keeping inflation in check. Image: Bloomberg

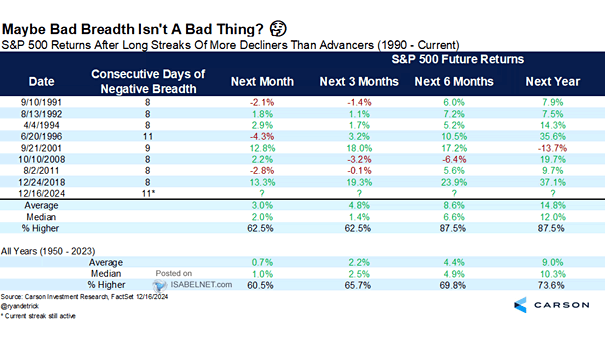

S&P 500 Returns After Long Streaks of More Decliners than Advancers Bulls have reason for optimism: since 1990, after long streaks of more decliners than advancers, the S&P 500 has been positive 87.5% of the time over the following 12 months, with an average gain of 14.8%. Image: Carson Investment Research

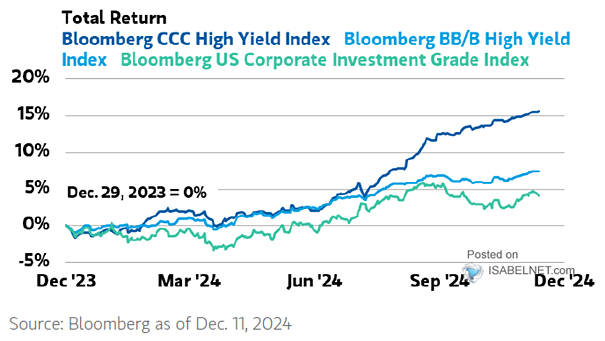

High-Yield Bond Returns 2024 has proven to be a terrific year for low-quality high yield investments, particularly within the CCC-rated cohort, which has seen returns exceeding 16%, as economic resilience exceeded expectations. Image: Morgan Stanley Wealth Management

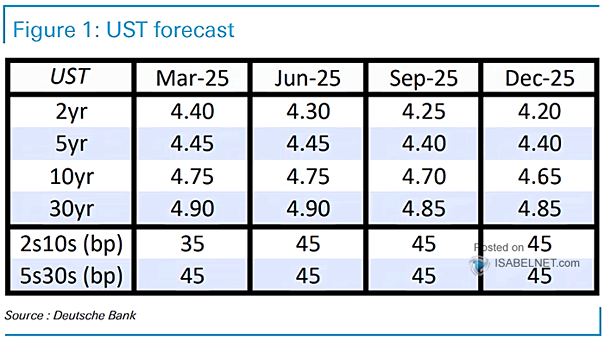

U.S. Rates – Treasury Yield Forecasts Deutsche Bank forecasts the 10-year UST yield at 4.65% by year-end 2025, driven by potential increased tariffs, fiscal easing and deregulation, which may lead to stronger economic growth and higher inflation. Image: Deutsche Bank

ISABELNET Cartoon of the Day With the S&P 500 hitting record highs, it’s time for a mass bear deportation—after all, they clearly missed the memo that this party is strictly bull-only! Have a Great Day, Everyone! 😎

Fed Funds Futures The market has scaled back its outlook for Fed rate cuts in 2025, with current projections showing three cuts, down from earlier forecasts. Image: Bloomberg