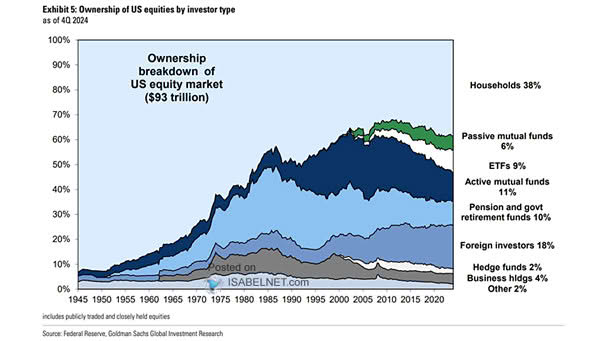

Ownership Breakdown of the U.S. Equity Market

Ownership Breakdown of the U.S. Equity Market (Share of Corporate Equity Market) U.S. households hold 40% of the U.S. equity market—a show of faith in stocks. Trouble is, nearly 90% of that sits with the richest 10%. Image: Goldman Sachs Global Investment Research