Probability of U.S. Recession Over Next 12 Months

Probability of U.S. Recession Over Next 12 Months The probability of U.S. recession over the next 12 months based on economic indicators stands at 45.6%. Image: J.P. Morgan

Probability of U.S. Recession Over Next 12 Months The probability of U.S. recession over the next 12 months based on economic indicators stands at 45.6%. Image: J.P. Morgan

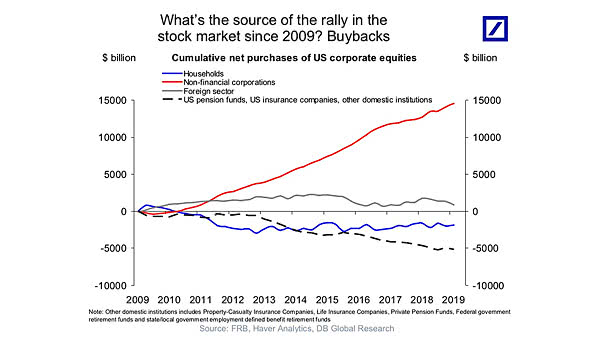

Buybacks Are the Source of the Rally in the Stock Market since 2009 But as trade tensions and economic slowdown worry U.S. firms, stock buybacks declined last quarter. Image: Deutsche Bank Global Research

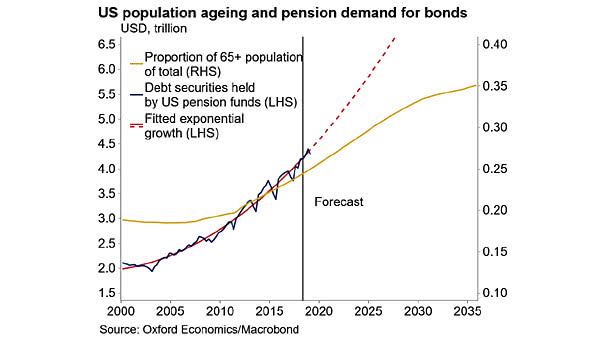

Demographics – U.S. Population Aging and Pension Demand for Bonds This chart suggests that U.S. pension demand for bonds is going to increase, as the proportion of 65+ rises. Image: Oxford Economics, Macrobond

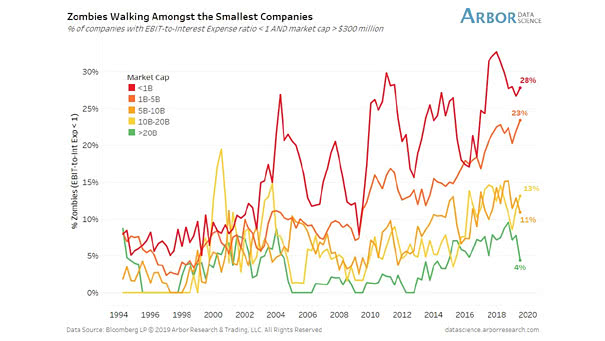

Zombies Walking Amongst the Smallest Companies Interesting chart showing the rise of zombie companies and their market capitalization. Image: Arbor Research & Trading LLC

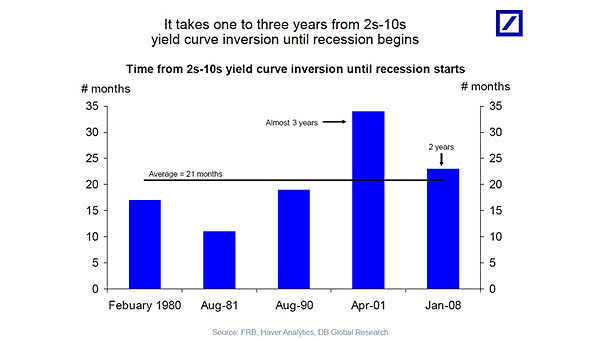

Time from 2s-10s Yield Curve Inversion until Recession Starts Recession tends to start in one to three years after the yield curve inversion. The yield curve is only one indicator among others of an economic puzzle. Image: Deutsche Bank Global Research

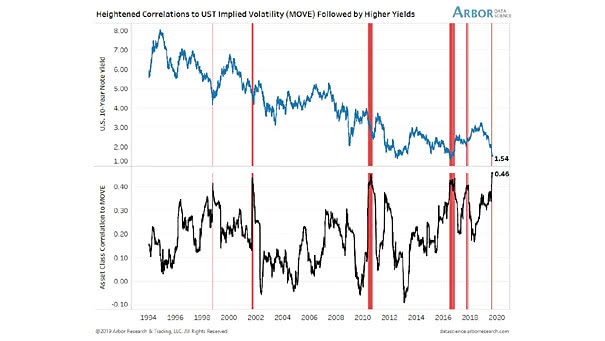

Heightened Correlations to U.S. Treasury Implied Volatility (MOVE) Followed by Higher Yields This chart suggests that balanced portfolios could suffer as U.S. Treasury yields generally rise after heightened correlation. Image: Arbor Research & Trading LLC

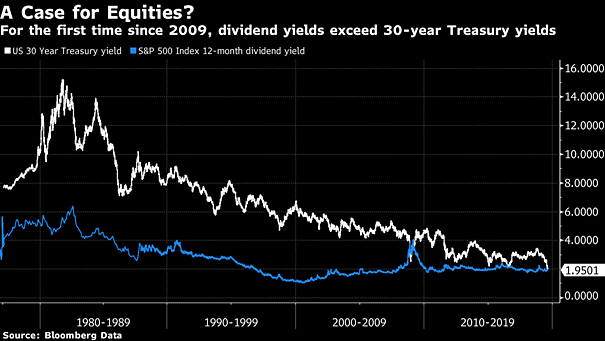

S&P 500 Dividend Yield and 30-Year Treasury Bond Are U.S. equities a “buy”? The dividend yield of the S&P 500 Index is now higher than the yield from a 30-year Treasury bond. This is a rare phenomenon. But the equity risk does not disappear because a company pays a dividend. Image: Bloomberg

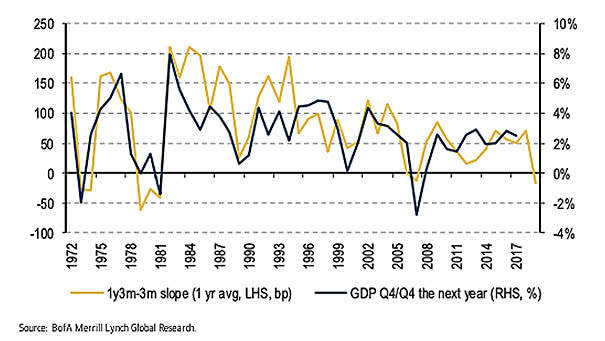

3-Month Rate 1-Year Forward vs. 3-Month Leads U.S. GDP This chart suggests that the 1y3m-3m slope leads U.S. GDP. The 1y3m-3m slope has turned down sharply and is informative for year-head growth. Image: BofA Merrill Lynch

The World’s Biggest Importers The U.S. is the largest importer in the world, followed by China and Germany. You may also like “The World’s Biggest Exporters.” Image: howmuch.net

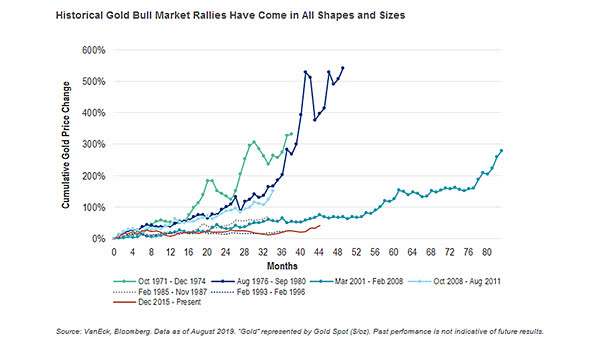

Historical Gold Bull Market Rallies Is it the start of a new gold bull market? This chart shows gold bull markets rallies compared to the most recent. Image: VanEck

Impact of an Inverted Yield Curve: S&P 500 and U.S. Dollar History tells us that the U.S. dollar and the S&P 500 could go higher, and the yield curve could stay inverted until mid-2020. Image: Nordea and Macrobond Click the Image to Enlarge