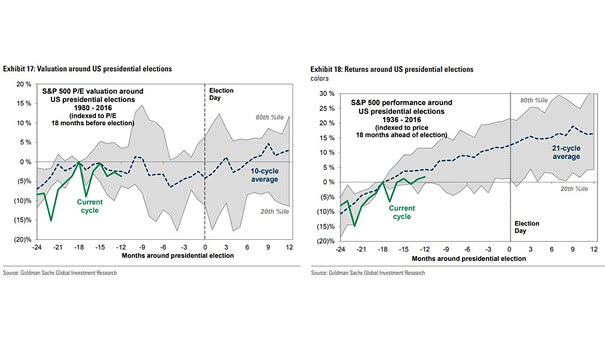

Valuation and Returns around U.S. Presidential Elections

Valuation and Returns around U.S. Presidential Elections Historically, the S&P 500 has performed well in the 12 months prior to an U.S. election. Image: Goldman Sachs Global Investment Research