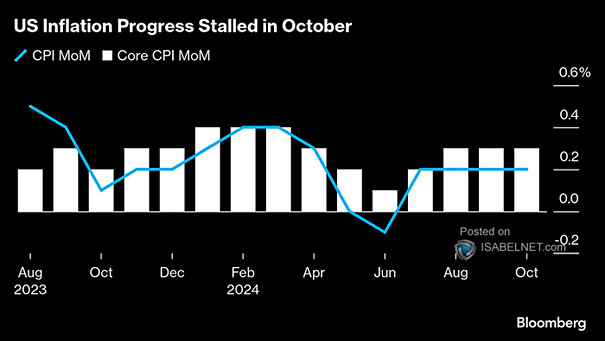

U.S. Headline and Core CPI Inflation

U.S. Headline and Core CPI Inflation The latest inflation data for October 2024 indicates that U.S. inflation has remained firm, showing a slight uptick rather than continuing its irregular descent, suggesting that the Fed’s battle against inflation is not yet over. Image: Bloomberg