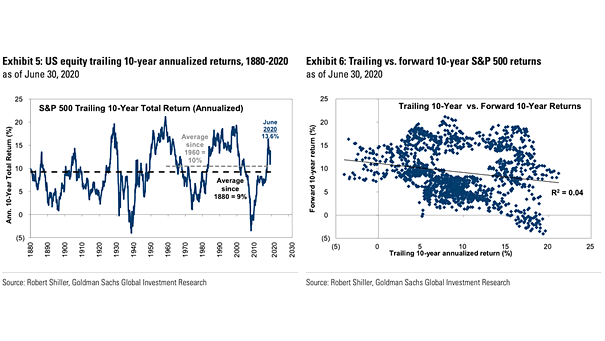

S&P 500 Trailing 10-Year Total Return vs. Forward 10-Year Returns

S&P 500 Trailing 10-Year Total Return vs. Forward 10-Year Returns Historically, forward 10-year S&P 500 returns are not correlated with trailing 10-year returns. Image: Goldman Sachs Global Investment Research