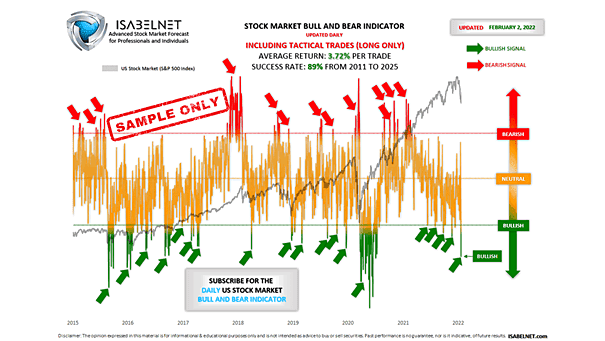

U.S. Stock Market Bull and Bear Indicator – S&P 500

U.S. Stock Market Bull and Bear Indicator – S&P 500 Friday, our Stock Market Bull & Bear Indicator was bullish well before the opening bell, and the S&P 500 followed through, ending the day up 0.62%. Using multiple financial data, this great model helps investors navigate through different market conditions. It suggests whether the U.S.…