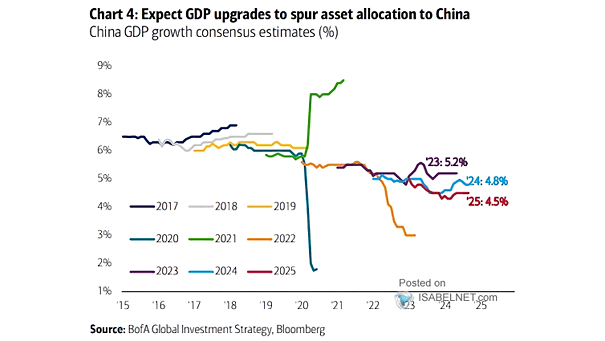

China GDP Growth Consensus Estimates

China GDP Growth Consensus Estimates GDP upgrades are likely to spur interest in China’s markets, encouraging asset allocation towards sectors that align with the country’s economic transformation. Image: BofA Global Investment Strategy