The Bull Market Has More to Run

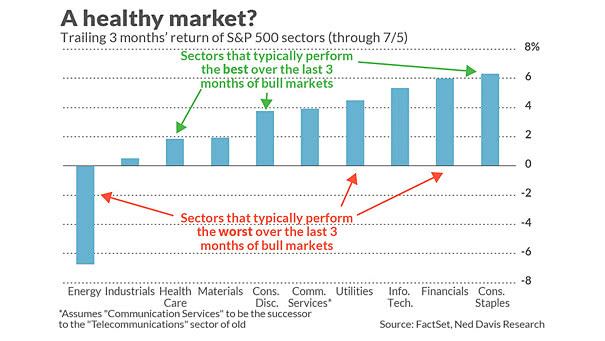

The Bull Market Has More to Run Sectors that typically perform the worst prior to market tops are holding up well. Image: MarketWatch

The Bull Market Has More to Run Sectors that typically perform the worst prior to market tops are holding up well. Image: MarketWatch

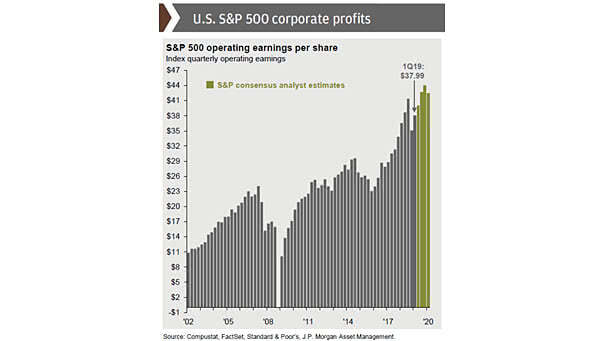

S&P 500 Operating Earnings per Share The S&P 500 quarterly operating earnings per share are Standard & Poors consensus analyst expectations as of 30 June 2019. Picture Source: J.P. Morgan Asset Management

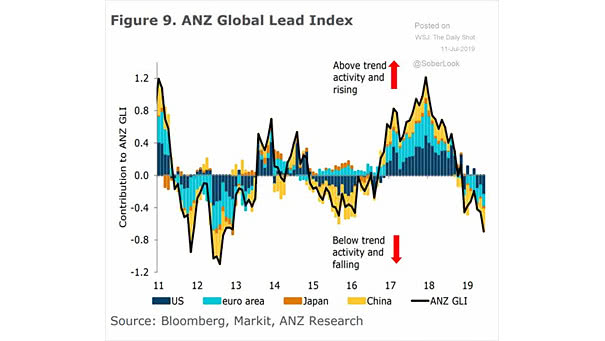

ANZ Global Lead Index The ANZ Global Lead Index is a leading indicator on global industrial production. The chart shows that growth momentum peaked in 2018. Currently, global growth is actually starting to moderate seriously. Image: ANZ Research

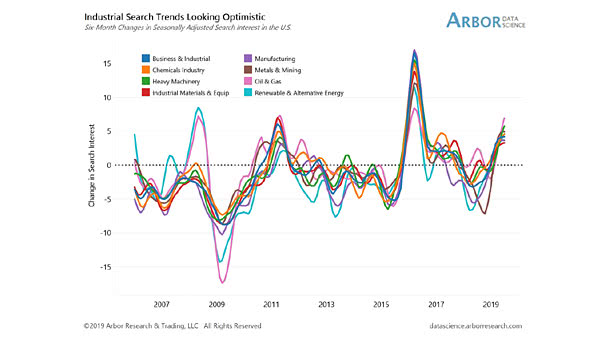

Industrial Search Trends Looking Optimistic This chart shows the rise in search interest in the U.S.. That’s good news after a fall in 2018, because industrial search trends tend to lead realized growth by a decent margin. Image: Arbor Research & Trading LLC

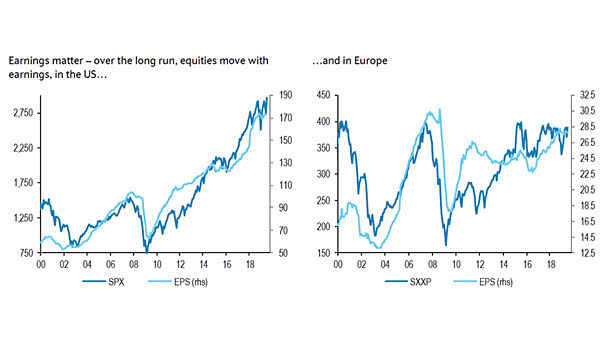

Earnings Matter, Over the Long Run Over the long run, equities move with earnings. Currently, there is a big gap between U.S. and Europe earnings. As Warren Buffett said: “for 240 years, it’s been a terrible mistake to bet against America.” You may also like “Global Earnings since 2006.” Image: Cullen Roche

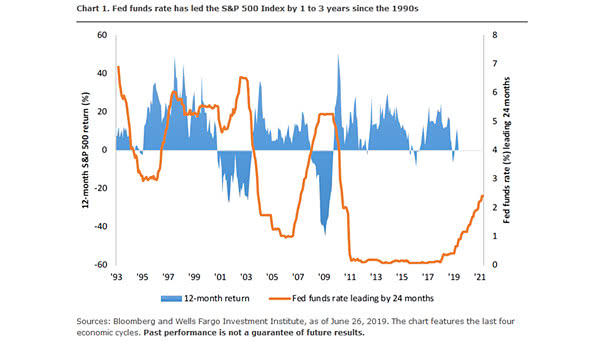

Fed Funds Rate vs. S&P 500 This chart suggests that the Fed funds rate leads the S&P 500 by 1 to 3 years since the 1990s. Image: Wells Fargo Investment Institute

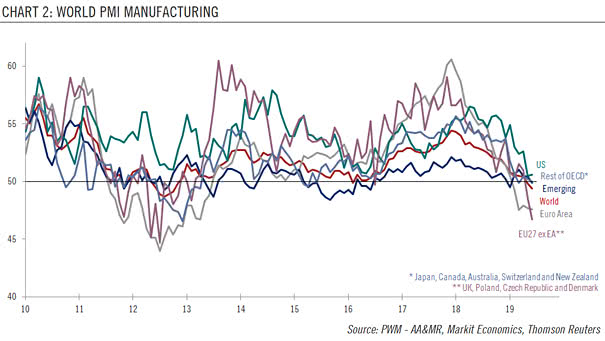

World PMI Manufacturing Most regions are now in contraction territory, except the United States. Image: Pictet Wealth Management

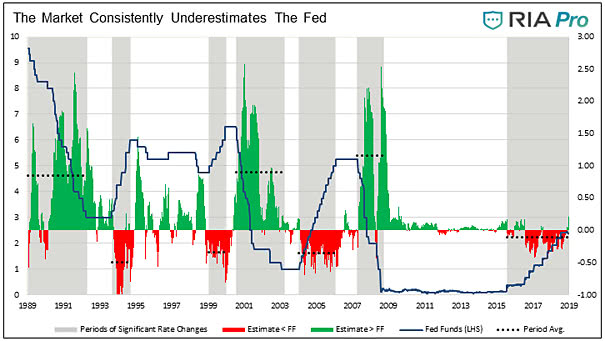

The Market Consistently Underestimates the Fed Usually, the Fed decides when to raise rates and the market decides when to cut rates. But, this interesting chart shows that the market consistently underestimates the Fed. You may also like “The Market is Almost Wrong about What the Fed Will Do.” Image: Real Investment Advice

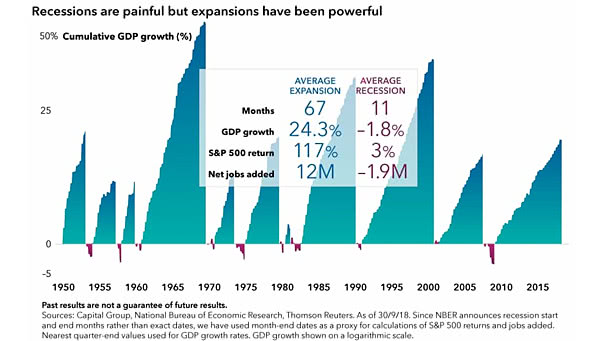

Economic Impact of U.S. Recessions This chart shows that the economic impact of most U.S. recessions is relatively small. The average expansion increased GDP by +24% vs. S&P 500 +117%, and the average recession reduced GDP by less than 2% vs. S&P 500 +3%. The average expansion is 67 months and the average recession is…

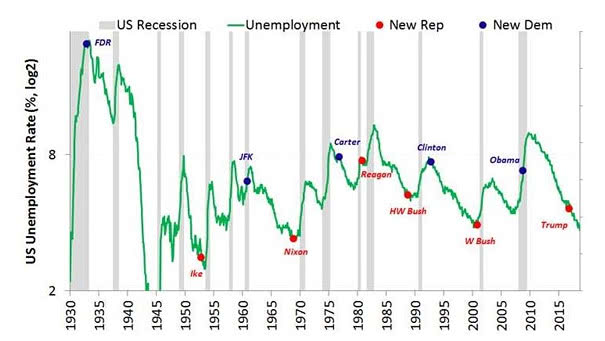

Unemployment and U.S. Presidential Elections Americans tend to elect Democrats when unemployment is high, and Republicans when unemployment is low. Image: Ken Fisher

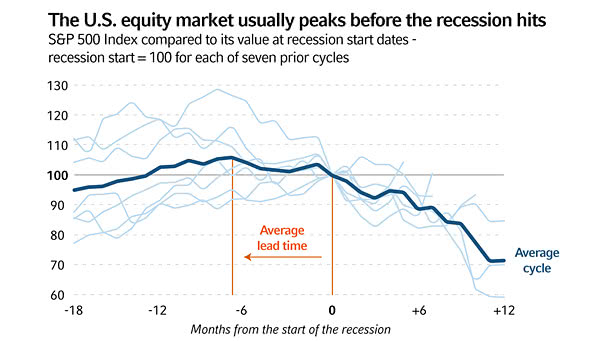

S&P 500 Performance Before and After Recessions since 1970 U.S. equities peaked about six months before the recession began. Image: Russell Investments