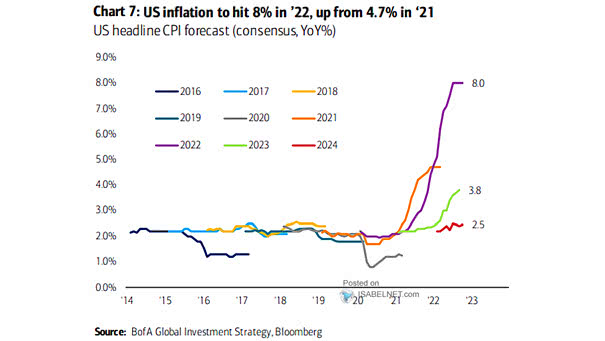

Inflation – U.S. CPI Deviation from Consensus

Inflation – U.S. CPI Deviation from Consensus A series of lower-than-expected inflation readings gives the administration greater economic leeway to pursue higher tariffs, driven by the (possibly mistaken) belief that U.S. consumers will be largely insulated from their effects. Image: Deutsche Bank