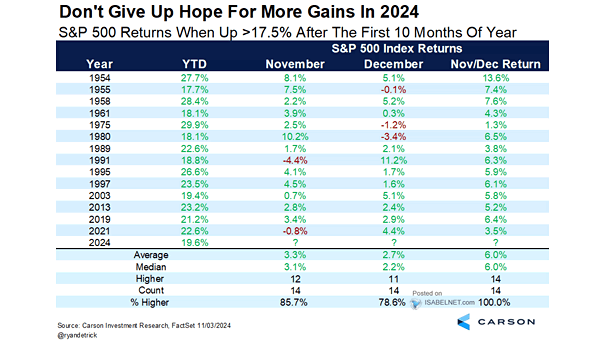

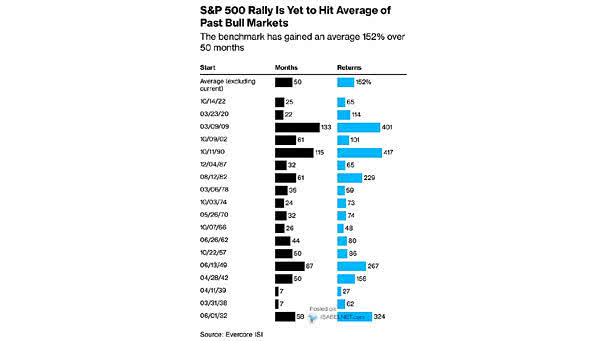

Percentage Change in S&P 500 in Previous Bull Markets

Percentage Change in S&P 500 in Previous Bull Markets The current bull market appears to be in its early stages, with historical data supporting the potential for significant gains in the coming months and years. Image: Bloomberg