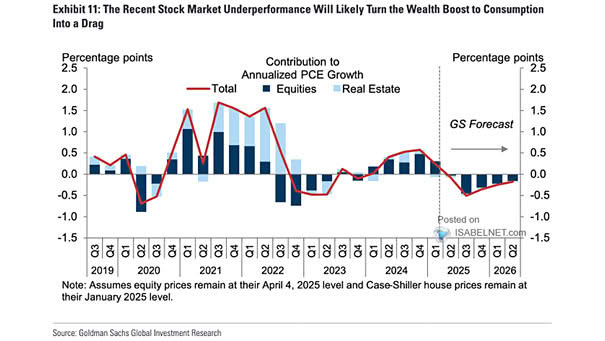

Estimated Wealth Effects on Annualized Real PCE Growth

Estimated Wealth Effects on Annualized Real PCE Growth Should stocks stumble, the positive wealth effect supporting consumption may turn into a headwind during the second half of 2026. After all, consumer sentiment is definitely tied to market performance. Image: Goldman Sachs Global Investment Research