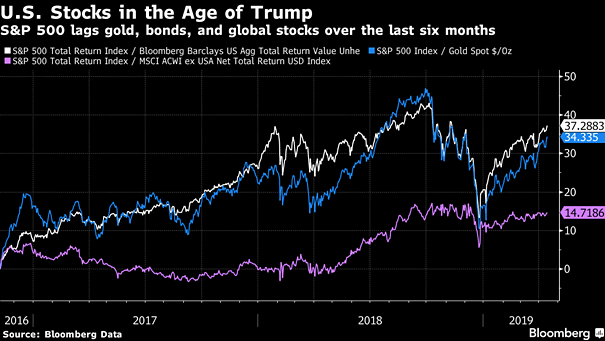

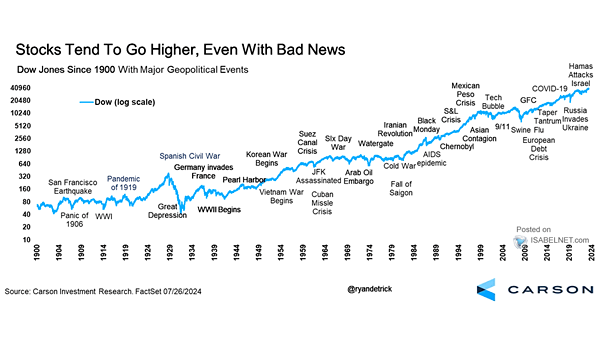

Stocks – Dow Jones with Major Geopolitical Events

Stocks – Dow Jones with Major Geopolitical Events Major geopolitical events can jolt markets, but U.S. equities have kept climbing as investors look beyond the headlines, rewarding those who stayed the course. Image: Carson Investment Research